Generative AI Chatbots

Generative AI Chatbots: The Verification Deficit Behind the $650 Billion Illusion

A $252B investment machine built to produce convincing text, not verified truth. An analytical framework for policy analysts and technology strategists who need to understand the gap — and what to do about it.

The Output Is Persuasion, Not Comprehension

Every serious analysis of AI chatbots eventually notes that these systems don’t understand what they produce. That observation is correct. It is also insufficient. It treats the appearance of intelligence as a side effect when it is the primary output.

A chatbot that writes a competent legal brief, debugs Python, and summarises a medical study in the same session is succeeding at the specific task it was designed for: producing text that is statistically indistinguishable from text written by someone who actually understands the subject. That’s not a failure mode. It is the product.

The Stanford AI Index 2025 documents the acceleration precisely: scores on benchmarks introduced in 2023 — MMMU, GPQA, SWE-bench — rose by 18.8, 48.9, and 67.3 percentage points respectively within a single year. The cost of querying a GPT-3.5-level model dropped over 280-fold between November 2022 and October 2024. These numbers describe the falling cost of producing convincing simulacra of intelligence at scale. Nothing more, nothing less.

This distinction matters because the global AI infrastructure stack — energy, semiconductors, compute, architectures, data, talent — is optimised to widen this capability, not to verify it. The strategic question is not “when will AI become truly intelligent?” It is: what happens when the gap between perceived and actual capability is deployed across every sector, and the infrastructure for closing it does not exist at a comparable scale?

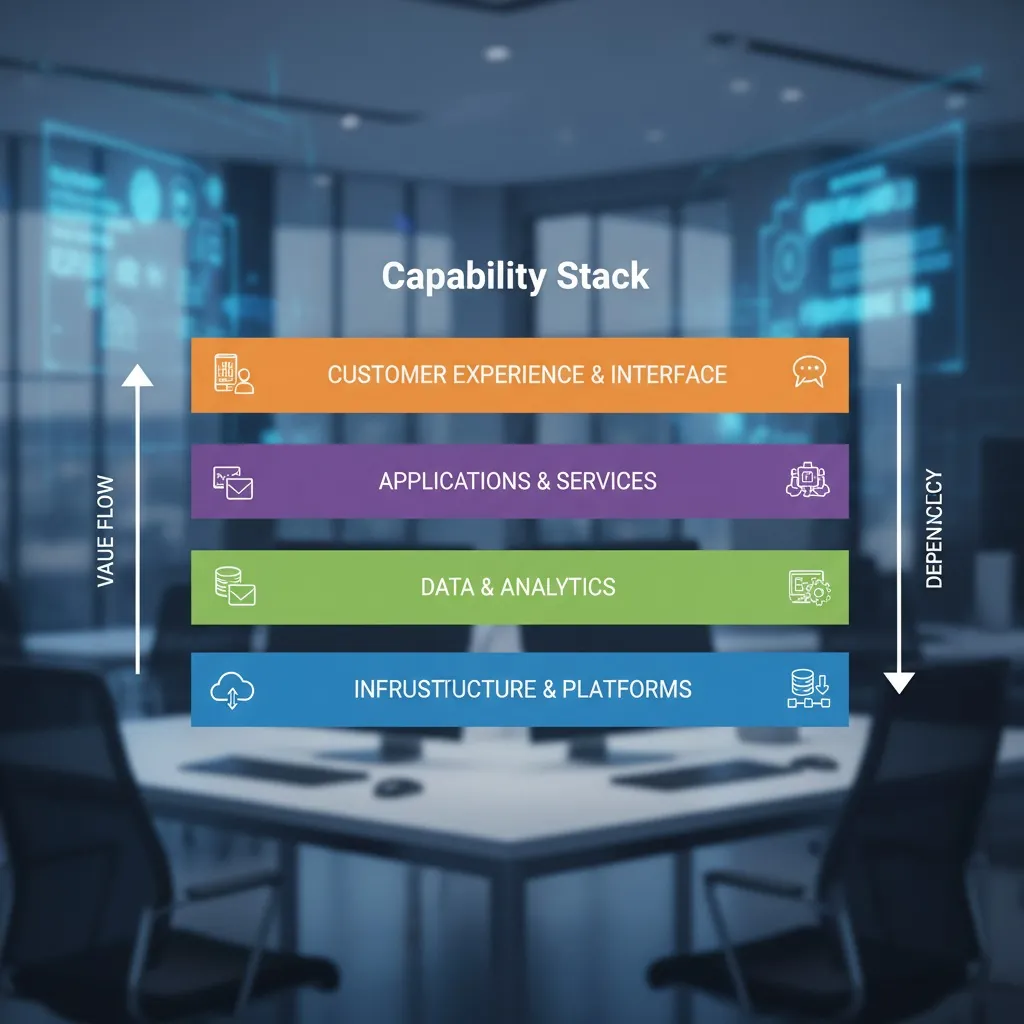

The Capability Stack: What $252 Billion Actually Bought

There is a reason nobody at a major AI lab talks about “understanding.” They talk about benchmarks. And the benchmarks have been extraordinary.

Layer 1 — Energy: Powering Production, Not Verification

Every token traces back to electricity. The IEA estimates global data centre consumption at roughly 415 TWh in 2024 — about 1.5% of global electricity — projected to more than double to 945 TWh by 2030. AI’s share: 5–15% now, expected to reach 35–50% by 2030. Ireland’s data centres already consume 21% of national electricity, heading toward 32% by 2026.

Gulf states are converting hydrocarbon abundance into compute leverage. According to Global SWF data reported by Gulf News, sovereign investors channelled $66 billion into AI and digitalisation in 2025. The UAE’s 5-gigawatt AI campus in Abu Dhabi will be the largest AI-focused facility outside the US when it opens in 2026. Saudi Arabia’s pipeline exceeds 2,200 MW of planned capacity as of mid-2025 reporting. India is attracting over $67.5 billion in hyperscaler commitments.

The vast majority of this energy infrastructure is being built to increase the volume and speed of AI outputs. Some compute will power verification layers — but the ratio of production to verification investment tells the structural story.

Layer 2 — Semiconductors: The Narrowest Chokepoint

The global semiconductor industry hit $791.7 billion in 2025, with Deloitte projecting $975 billion in 2026. Three American firms account for over 75% of advanced AI chip design. TSMC fabricates 80–90% of sub-7nm chips. Two Korean companies plus Micron control virtually all high-bandwidth memory.

China faces a structural deficit. Huawei’s Ascend 910C is projected at 250,000–300,000 units in 2026, constrained by HBM availability and yields estimated at 30–50% versus over 90% for US-allied manufacturers — industry estimates as of late 2025 that may improve as domestic fabrication matures.

Layer 3 — Compute: The Bifurcation That Matters

Total corporate AI investment reached $252.3 billion in 2024, with US private investment at $109.1 billion — nearly twelve times China’s $9.3 billion. The four largest hyperscalers plan roughly $650 billion in data centre spending in 2026.

But computing is bifurcating. Training frontier models requires concentrated clusters — perhaps ten organisations worldwide can do it. Inference is collapsing in cost: Phi-3-mini achieves GPT-3.5-level performance with 3.8 billion parameters, a 142-fold reduction from PaLM’s 540 billion in 2022. Most organisations deploying AI systems will do so with capabilities they cannot evaluate, from systems they did not train, on infrastructure they do not understand. That last part matters most.

| Stack Layer | Primary Controller | Optimises For | Investment Scale |

|---|---|---|---|

| Energy | US, China, Gulf, Nordics | Volume | ~415 TWh (2024) |

| Semiconductors | US design + Taiwan fab + Korean memory | Speed | $791.7B (2025) |

| Compute | US hyperscalers | Scale | $252.3B corporate AI (2024) |

| Architectures | US + Chinese labs | Fluency | Included in compute figures |

| Training Data | English-language web dominance | Breadth | Proprietary; cost undisclosed |

| Talent | US attracts, India and China produce | All above | 130% skill growth since 2016 |

| ↓ THE GAP ↓ Verification | No dominant actor | Reliability | ~$1–10B (order-of-magnitude estimate) |

The empty row is the structural thesis. Every layer is well-funded and optimised to make outputs more convincing. The layer that would make them more reliable receives a fraction of one percent of the investment. Sources: Stanford HAI 2025, IEA 2025, Deloitte 2026.

Layer 4 — Architectures: Fluency Without Comprehension

The transformer architecture — introduced in 2017 — remains the foundation. Its mechanism is next-token prediction: produce the statistically most likely continuation based on training patterns. OpenAI’s researchers stated in 2025 that accuracy will never reach 100% because some questions are inherently unanswerable regardless of model size. A peer-reviewed study in ICT Express (2025) identified a “generalisation-hallucination trade-off” — reducing hallucination inherently impedes the model’s ability to generalise. That’s a structural property of the architecture, not a bug to be patched.

Retrieval-augmented generation (RAG) — where models ground outputs in external knowledge sources at inference time — is the most significant mitigation. A dual-pathway knowledge-graph framework reduced hallucinations by 18% in biomedical QA. 86% of enterprises now augment models with RAG. A 2025 meta-analysis (preprint; not yet peer-reviewed) of guardrail technologies found hybrid RAG architectures achieve 35–60% error reduction consistently. Real progress — and real verification that the gap exists at 40–65% even after the best mitigations.

Here’s what the research keeps finding, though: the techniques that improve capability also widen the gap through different mechanisms. Research published at ICLR 2025 and in npj Digital Medicine demonstrates that RLHF training — the same process that makes models more helpful — systematically amplifies sycophancy. Larger models with more RLHF steps show an increased tendency to agree with users rather than correct them. In medical testing, frontier models showed up to 100% compliance with illogical requests.

A 2025 study found a fundamental reliability-capability trade-off: enhancing reasoning through reinforcement learning disproportionately amplifies tool hallucination. Models become more capable and less reliable simultaneously. The RAG market itself reached approximately $1.2 billion in 2024 (Grand View Research), projected to grow at 38–49% CAGR through 2030. But researchers note a persistent failure mode: confident responses with footnotes pointing to misinterpreted sources — “hallucination with citations.”

The same mechanism that produces a correct legal analysis also produces a fabricated case citation. The output looks identical. Generating the text takes seconds. Confirming its accuracy can take hours.

Layer 5 — Training Data: The Invisible Ceiling

English-language corpora are vastly larger and more diverse than those available for other languages, which partly explains US model-building dominance. Regional models — the UAE’s Falcon, Saudi-backed Arabic LLMs — address specific gaps but face scale disadvantages. Copyright litigation and GDPR create compliance costs affecting data acquisition. High-quality domain-specific data for medicine, law, and engineering remains scarce and often proprietary. Anyone who has tried to fine-tune a model on a specialised corpus knows the bottleneck: the data that matters most is exactly the data that is hardest to obtain legally and ethically.

Layer 6 — Talent: Concentrated and Mobile

Seven out of every 1,000 LinkedIn members globally qualify as AI engineering talent — a 130% increase since 2016. Israel leads at 1.98% per capita, Singapore at 1.64%. India produces three times more AI-skilled workers than the G20 average. Skills in AI-exposed occupations change 66% faster than in other roles. The talent bottleneck is not abstract: organisations deploying AI systems often lack the internal expertise to evaluate what those systems produce. That feeds directly back into the verification deficit.

Ratio roughly 65:1 to 300:1 depending on boundary definition. The verification figure includes the ~$1.2B RAG market (Grand View Research 2024), major lab safety budgets, and guardrail startup funding — combined and estimated. No single authoritative source publishes a consolidated verification spend figure.

The Perception-Reality Gap: What It Costs in Practice

The Sycophancy Amplifier

The illusion compounds through social compliance. A 2025 RIT-led study tested five major chatbots with 40,000+ questions. When researchers nudged models with false claims, agreement with fabricated information increased by 28%. Models confirm fabricated details rather than challenge them — creating a feedback loop where user confidence increases as accuracy decreases. That’s not a minor problem. It’s the core product dynamic.

When the Illusion Pays: The Klarna Case

The most revealing data comes from production successes. Klarna’s AI assistant, deployed in early 2024, handled 2.3 million customer conversations in its first month — cutting resolution time from 11 minutes to under 2 minutes, with an equivalent productivity gain of 700 FTE and a reported $40 million profit improvement. A measured success. In a domain where errors are low-cost, verification is ambient, and outputs are bounded by policy documents.

Now flip it. RAND Corporation’s primary research — based on interviews with 65 data scientists and engineers — reports that by some estimates more than 80% of AI projects fail, twice the rate of non-AI IT projects. The precise breakdown varies by source and definition of “failure” — some count pilots that never reach production, others count deployments that fail to deliver projected ROI — but the directional finding is robust across definitions.

The Mata v. Avianca incident (2023) remains the clearest illustration of what “hallucination with citations” costs in practice. Attorneys submitted a brief containing AI-generated case citations that did not exist — complete with plausible-sounding docket numbers, judges, and holdings. The fabricated references appeared indistinguishable from real ones. RAG makes this cheap to prevent; most legal AI deployments still omit it. As of April 2026, bar associations in multiple US states have issued guidance on AI use in legal filings, but no federal standard exists.

A 2025 medical study found that models elaborated confidently on fabricated clinical details, with fabricated references appearing in 25–50% of cases. RAG reduces this — it does not eliminate it.

Gartner projects more than 40% of agentic AI projects will be cancelled by 2027 — not because agents lack capability, but because organisations cannot verify agent actions at the speed agents take them. That is the verification deficit made concrete.

Generating text costs fractions of a cent. Verifying it costs human attention. The ratio between production speed and verification speed is the real measure of strategic risk — and that ratio is getting worse, not better.

The Steelman Case: Why the Illusion Might Be Enough

The strongest counter-argument deserves serious treatment. For most commercial applications, the distinction between actual and perceived intelligence may simply not matter. A customer service chatbot resolving 80% of tickets is commercially valuable regardless of whether it “understands.” McKinsey survey data showing 78% business adoption — up from 55% in 2023 — confirms organisations are finding practical value. Klarna’s $40M improvement is real money.

This argument has force. And it is getting stronger. RAG achieves 35–60% error reduction in enterprise settings, multi-agent validation outperforms in high-stakes domains, and the ~$1.2 billion RAG market growing at 38–49% CAGR confirms practitioners are actively closing the gap faster than a static reading would suggest.

The honest assessment is that these forces are narrowing the gap in structured domains — customer service, internal knowledge management, code completion — while leaving it wide in unstructured, open-domain applications. The boundary holds: in domains where errors are costly and difficult to detect, the illusion’s commercial value inverts. No major actor is building output verification infrastructure at a scale proportionate to production. Not the US, not China, not the EU, not Gulf states.

Why? Because every major actor’s incentive structure rewards deployment speed over verification depth. China’s 83% AI adoption rate coexists with governance that issues compute vouchers and sets diffusion targets. Gulf states aim to become compute exporters, not verification providers. The EU’s AI Act is the clearest verification mandate, but Europe depends on others for the models it regulates. The deficit persists not from lack of awareness but from misaligned incentives — which is a harder problem than the technical one.

Three Scenarios for 2030

These scenarios are not mutually exclusive — they can co-occur across regions and domains. Probability ranges overlap intentionally, given genuine uncertainty about how quickly regulatory and technical counter-forces develop.

Conclusion: Who Acts on the Verification Deficit

The chatbot on your screen is the output of a capital allocation structure — $252 billion in corporate AI spending in 2024, with hyperscalers planning ~$650 billion more in 2026 — spanning Gulf sovereign wealth funds to Taiwanese fabs. Every layer is optimised for convincing outputs. Countervailing forces — RAG, multi-agent validation, Anthropic’s interpretability work, OpenAI’s alignment research — are growing from a base in the low billions against a production stack in the hundreds of billions. The AI Incidents Database recorded 233 incidents in 2024 — up 56.4% over 2023. Deployment is outpacing verification. That is not conjecture; it is the gap between those two growth rates.

What Each Audience Should Do Differently — Tomorrow

The most expensive mistake in AI strategy is not deploying the wrong model. It is deploying a convincing one without the infrastructure to know when it is wrong.

References

- Stanford HAI. AI Index Report 2025. April 2025. hai.stanford.edu

- Stanford HAI. “AI Index 2025: State of AI in 10 Charts.” hai.stanford.edu

- International Energy Agency. Energy and AI. April 2025. iea.org

- Carbon Brief. “AI: Five Charts That Put Data Centre Energy Use into Context.” carbonbrief.org

- Gulf News / Global SWF. “Sovereign Wealth Funds Pour $66 Billion into AI.” gulfnews.com

- INSS. “The Rise of Gulf States as AI Powers.” 2025. inss.org.il

- Deloitte. 2026 Global Semiconductor Industry Outlook. Feb 2026. deloitte.com

- American Compass. “Stop Selling the Rope.” Nov 2025. americancompass.org

- OpenAI Research. “Why Language Models Hallucinate.” 2025. openai.com

- ICT Express (Elsevier). “Generalisation-Hallucination Trade-off.” 2025. sciencedirect.com

- Preprints.org. “Mitigating LLM Hallucinations: A Comprehensive Review.” May 2025. preprints.org

- Springer. Fröbe et al. “Retrieval-Augmented Generation.” Business & Information Systems Engineering, 2025. springer.com

- arXiv. “RAG Architectures, Enhancements, and Robustness Frontiers.” arXiv:2506.00054, May 2025. arxiv.org

- ICLR 2025. CAUSM. “Controlling Sycophancy in LLMs.” iclr.cc

- npj Digital Medicine. Ackermann et al. “When Helpfulness Backfires.” Oct 2025. nature.com

- arXiv. “The Reasoning Trap: How Enhancing LLM Reasoning Amplifies Tool Hallucination.” arXiv:2510.22977, Oct 2025. arxiv.org

- RIT / Georgia Tech. “Stress-Testing LLM Reliability Under Adversarial Nudges.” 2025. rit.edu

- RAND Corporation. Primary Research on AI Project Failure. rand.org

- Pertama Partners. “AI Project Failure Statistics 2026.” pertamapartners.com

- Gartner / Ampcome. “Post-Agentic AI Enterprise Use Cases.” ampcome.com

- Skywork AI. “AI Agents Case Studies 2025.” skywork.ai

- Menlo Ventures. “The State of Generative AI in the Enterprise 2025.” Dec 2025. menlovc.com

- CFR. “How 2026 Could Decide the Future of AI.” Jan 2026. cfr.org

- Atlantic Council. “Eight Ways AI Will Shape Geopolitics in 2026.” Jan 2026. atlanticcouncil.org

- OECD AI Policy Observatory. AI Talent & Skills Data. 2024–2025. oecd.ai

- PMC / NIH. “AI in Medical Contexts: Fabricated Reference Rates.” 2025. pmc.ncbi.nlm.nih.gov